Fintech needs more regulation

Fintech needs more regulation.

I also predict the F-Prime Fintech Index will bounce back.

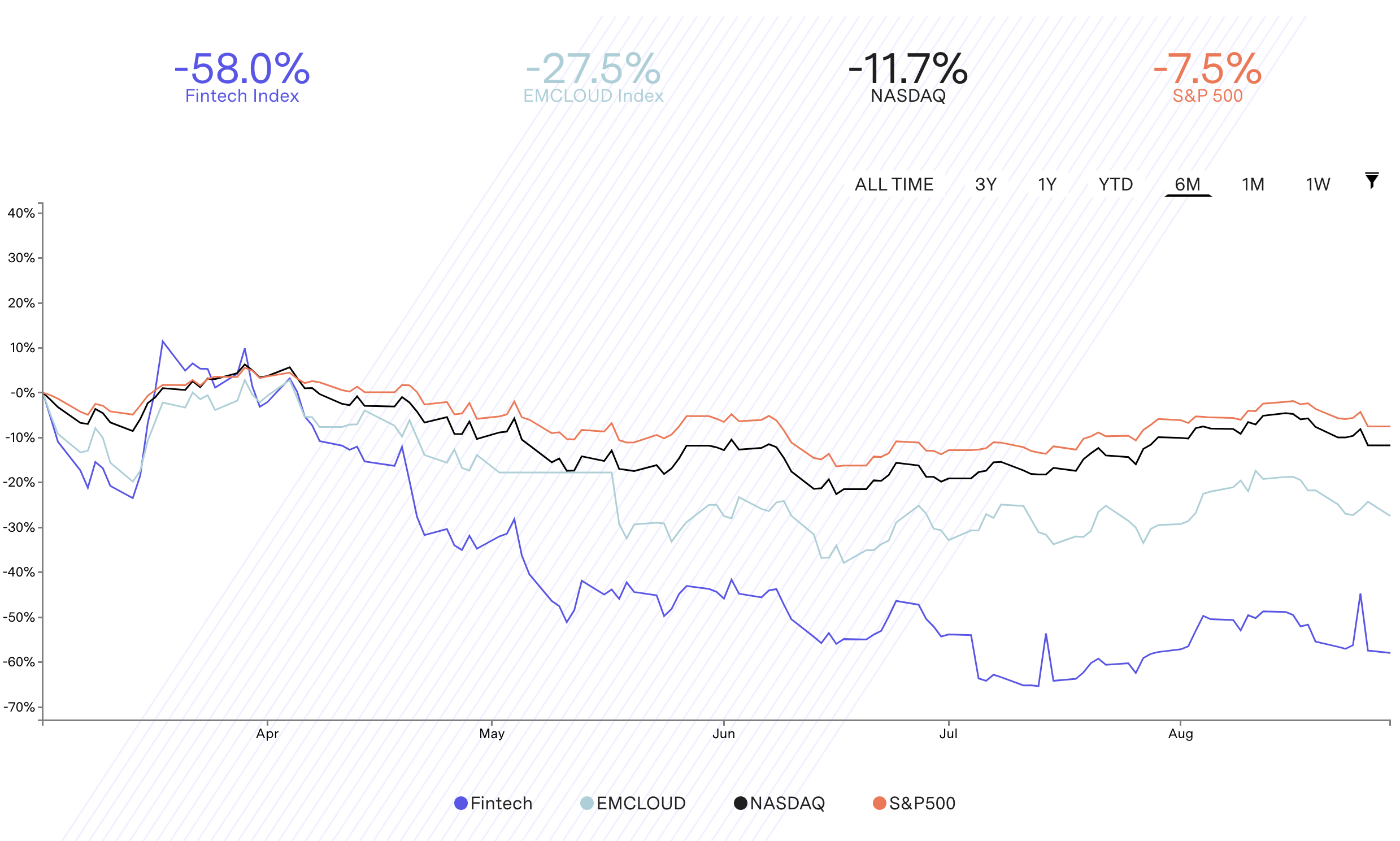

In the last six months, the fintech sector went through the largest decline in value since fintechs existed. The F-Prime Fintech Index, a basket of publicly traded financial technology companies like Paypal, has lost 60% since March 2022. That’s a lot.

More interestingly, the recent turmoil shed some light on the kind of love-hate relationships financial technologies have with regulation. We are seeing more and tougher actions from regulators on fintechs. While some see this as a signal that the fintech party is over, I actually think it is a very good sign and fintech will bounce back higher if the regulators keep applying pressure here.

Full disclosure: I am a ex-fintech founder who has been through (and came clear of) an investigation by the French regulator. I wouldn’t go through it again. I am naturally inclined for less regulation.

More regulation, more pain?

Have a look at crypto platforms and FDIC insurance. Voyager customers just found out their deposits were not insured against Voyager bankruptcy. Have a look at Klarna slashing its valuation from $46 bn to $6 bn. British BNPL providers, who used to operate outside traditional credit regulation, are now regulated by FCA.

The last 6 months have seen tons of similar news showing how regulators are stepping up and taking fintechs more seriously. Maybe the F-Prime Fintech Index is down because of this. Maybe the index is down for other reasons. But I think regulators stepping up is a good thing. Fintech will bounce back higher because there is going to be more regulation.

I am not the only one to stand for more regulation: even Klarna’s head of UK is urging the Government to move quicker than planned to implement regulation. Now, why would someone be calling for more rules and processes on his / her own activity?

Bad apples harm everyone

Simply because it is good for business. By enforcing more stringent rules, regulators bring trust in the financial system. It protects the customer against financially dodgy schemes and non-legitimate players who are using financial technology to abuse people. When it is too hard for them to do business, scammers go away. Customers are less hacked. They use products without the fear of being robbed. And the flywheel of trust starts spinning. Regulations play a key role in ensuring that the industry develops in a healthy way for consumers to enjoy better access to financial services, which is the raison d’etre of fintech.

Klarna will withstand FCA new guidelines but the sketchy BNPL providers won’t.

I won’t make the same observation for Voyager though.

Fintechs first thrived against incumbents because they were somehow less regulated than their fully-fledged banking peers. But fintechs initial success also attracted not-so-well-intentioned people who used financial technology to lure customers into financially dodgy schemes that were not yet frauds per se. More stringent fintech regulation will weed out these players and be a net positive for the whole sector in the long term. It will help build up customer trust in financial technology. I think the current fintech downturn is oversold and I am optimistic about the future of the whole industry.

In the next posts, I will dive more into the scammers, and the scams, that have been made possible thanks to technology in financial services. I will also explore why regulation failed in some cases.